The Doom Loop Begins

The Japan Doom Loop Is No Longer a Theory

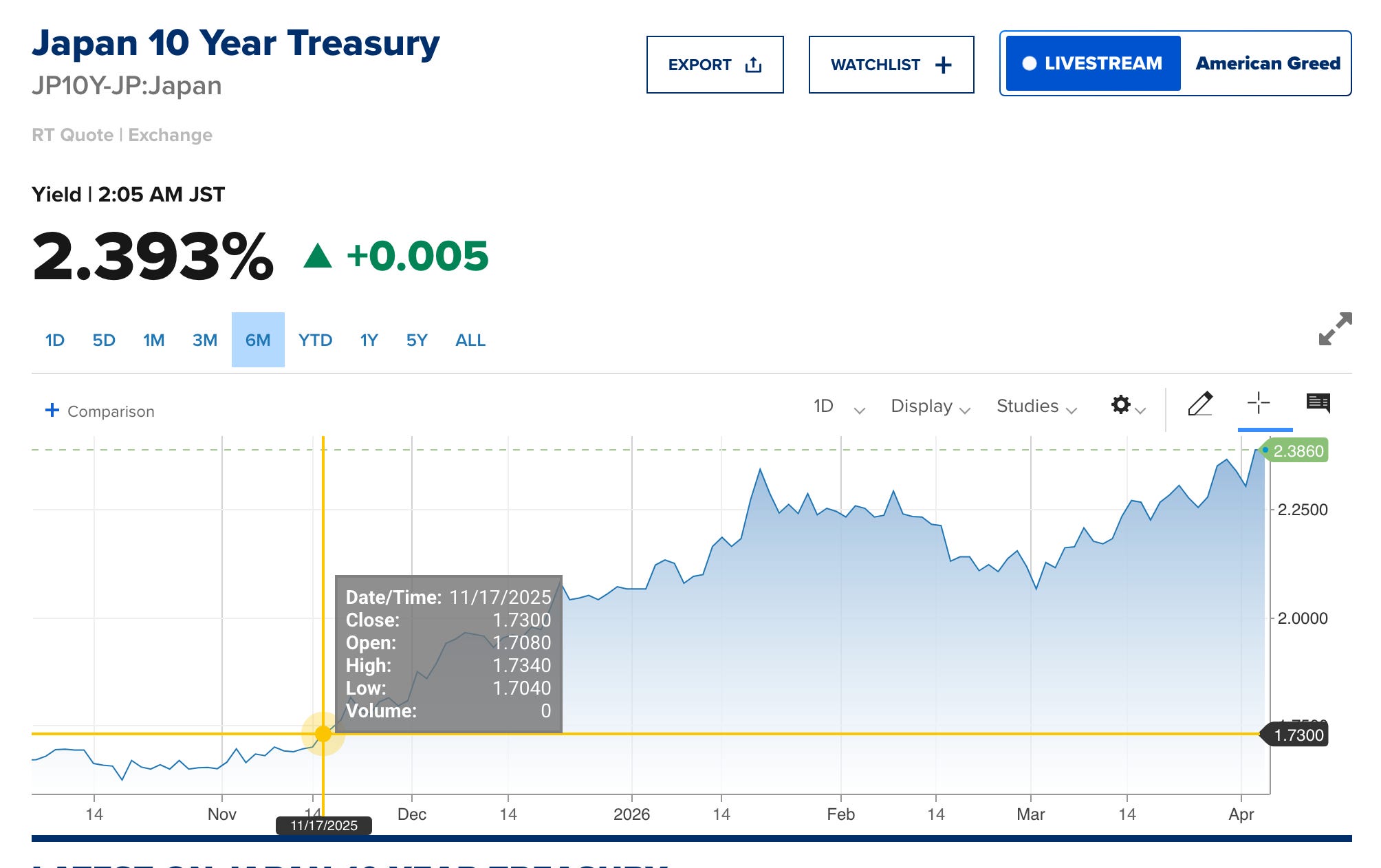

When I wrote about Japan’s bond market in November here:

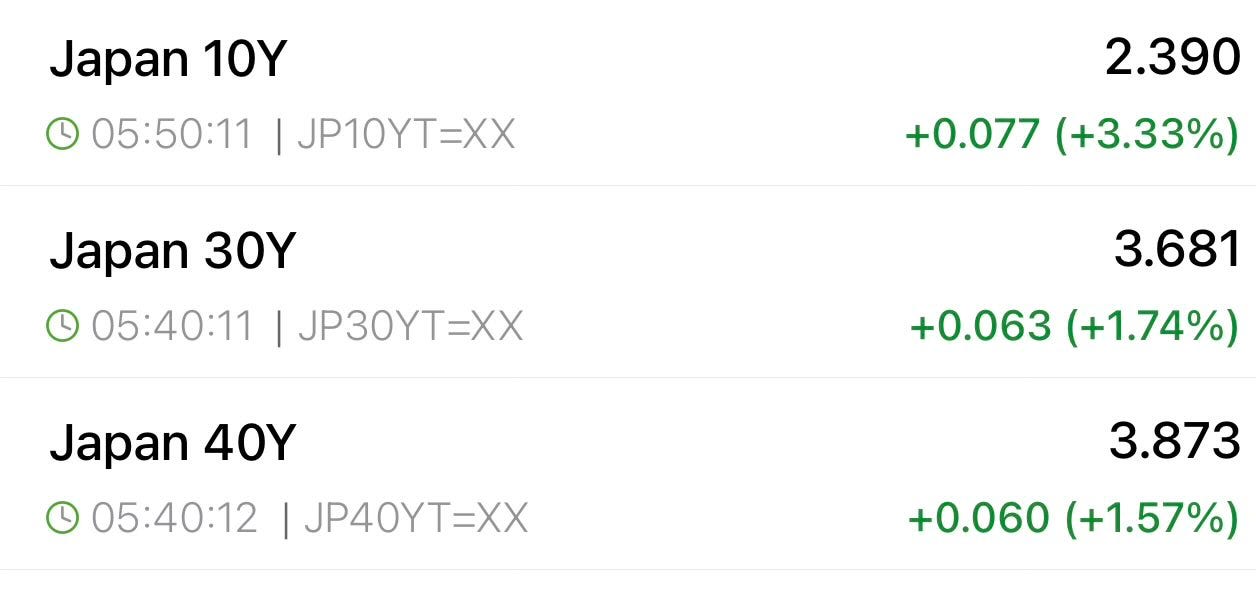

the 10-year yield sat at 1.71%, already the highest since 2008. It just hit 2.39%. The 30-year is at 3.68%. The 40-year at 3.87%. The doom loop I described isn’t approaching. It’s already running.

The Carry Trade Is Dying

For years, the math was simple for Japanese banks and institutions: borrow cheaply in yen, park the money in US Treasuries, and collect the difference. Positive carry, earning more on dollars than you’re paying out on yen. It was practically free money.

That trade is now closing. As the Bank of Japan keeps raising rates, the interest cost of holding yen debt is climbing. The spread that made US Treasuries so attractive is shrinking. And with the yen sitting near 160 to the dollar, Japanese institutions have a rare window. They get more yen back for every dollar they convert right now than they will if the yen recovers. Cashing out US Treasuries at this exchange rate is the best of a bad set of options.

The Treasury Selling Pressure Is Real

Japan holds roughly $1.2 trillion in US Treasuries. If even 10 to 15% of that gets repatriated, that’s $120 to $180 billion in selling pressure hitting US bonds, at exactly the moment the Fed cannot cut rates because oil driven inflation won’t allow it. When Japan sells, it floods the market with bonds that need new buyers. To attract those buyers, prices drop. And in the bond market, price and yield move in opposite directions. More selling equals lower bond prices equals higher US interest rates.

The US is running $2 trillion+ deficits and desperately needs foreign buyers to show up. Japan is the largest foreign holder of US Treasuries. China is second. Japan quietly stepping back removes the biggest pillar of demand at the worst possible time.

The proceeds don’t disappear either. Japan can use them to buy back its own government bonds from foreign holders, reducing the interest burden it owes outside its borders. Damage control, but at a direct cost to US Treasury markets.

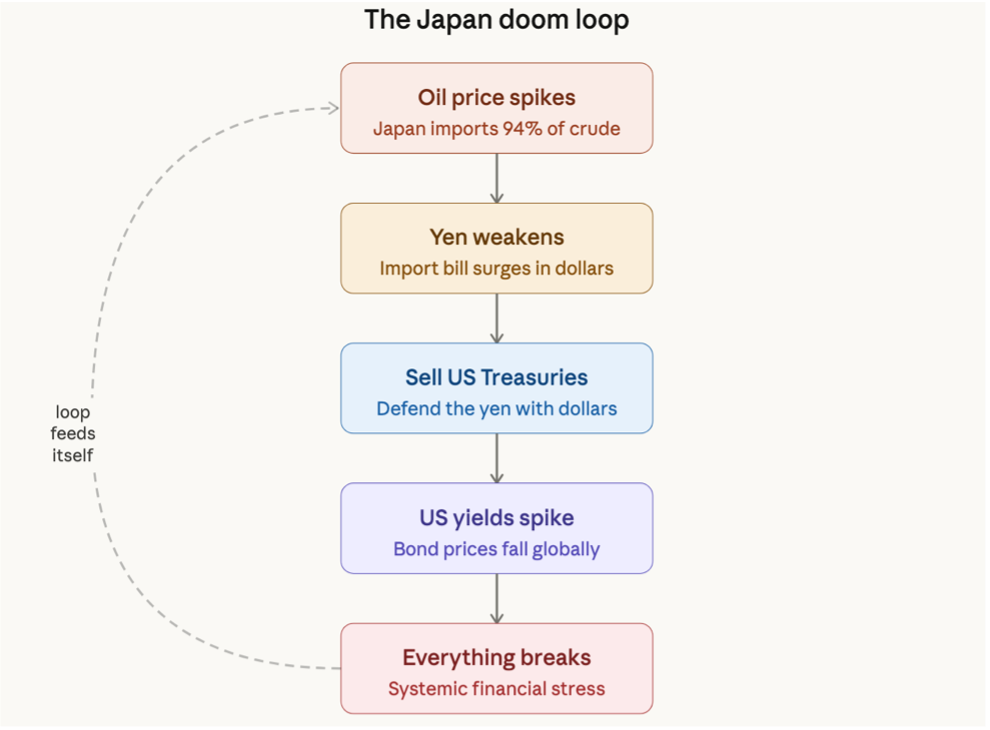

The Energy Wildcard

Japan imports 94% of its crude from the Middle East. 70% of it moves through the Strait of Hormuz. This is not a minor detail. It is the foundation of Japan’s entire industrial economy.

Any serious disruption to that supply route sends oil prices sharply higher. For Japan, that means a surging import bill paid in dollars, which puts immediate downward pressure on the yen. A weaker yen makes imports even more expensive, inflation climbs, and the Bank of Japan faces pressure to respond. The result is the same every time: more Treasury selling to defend the currency, more pressure on US bond markets, higher yields globally.

If oil prices spike from here, Japan’s import bill surges, the yen weakens further, and the pressure to sell Treasuries accelerates. The loop feeds itself

.

The Fiscal Trap

Japan’s government is running out of room to maneuver. Yields at these levels mean the cost of servicing its debt is rising fast, and Japan’s debt is already over 230% of GDP as per the IMF. The options on the table are all painful: raise taxes and slow an already fragile economy, cut government services, or print money to cover the gap. Printing money is self-defeating because it pushes inflation higher, which pushes yields even higher, which makes the debt burden worse. There is no clean exit. Every path forward tightens the loop further.

What This Means

Japan is caught between rising domestic rates, a weak currency, a carry trade that no longer works, and a debt load that is becoming harder to justify to bond markets by the day. Every pressure point I outlined in November has gotten worse. The bond yields are the market telling you it agrees.

Watch USD/JPY. Watch the 10 year. The next move in global markets may well start in Tokyo.